Poor Kid, Big Debt

My Journey to Deliberate Freedom

Growing Up Poor in the Ozarks

I grew up in rural Arkansas, down a dirt road in the Ozarks. We didn’t starve—my days started with milking our cow and tending the garden that kept us fed through winter with home-canned vegetables. But with six family members living on $10,000 a year in the 1980s, luxuries were nonexistent. No cable TV reached us, just two fuzzy broadcast channels. We had a “party line”—a shared phone line that was no party at all—with four families along the same dirt road, and the internet wasn’t even a concept in our isolated world.

Navigating Dead-End Jobs and Debt

My first costly decision came when I turned down a full scholarship in Arkansas—a state I couldn’t wait to escape—for school in Springfield, Missouri. Two failed semesters and a brief, unsuccessful stint in Navy boot camp later, I was 19 with student debt and no direction. Feeling trapped in a cycle of dead-end choices, I turned to whatever work I could find to keep myself afloat. Thus began the food service years—fast food, dive restaurant cook. This period was interrupted by a two-day telemarketing job I quit because the required half-truths they wanted me to tell people made me physically ill. These were the hungriest years of my life. There were no cows or vegetable gardens in town, and I remember eating expired food from the fast food joints where I worked or scrounging change to buy 25-cent packages of cookies from the convenience store.

With no clear career path in sight, I followed a girlfriend to Chapel Hill, North Carolina, where I reinvented myself, bouncing between temp jobs—receptionist, secretary, data entry, accounts payable. In that accounts payable department, as an early hint of what I’d do later, I created an Excel spreadsheet to speed up their paper-based reconciliation, making it faster and far more accurate. Around this same time, I went into debt for my first computer, having previously only typed programs from second-hand magazines into borrowed TI-99/4A and Commodore 64 machines.

New York Dreams and Reality

After our breakup, I lived briefly with relatives in New Jersey before landing bright-eyed and dream-filled in New York City—with no job and no prospects. I rented couch space for $200 monthly—and still bounced the check. When my housing fell through, I slept in my tiny Ford Ranger pickup (which got burgled while I was at work) for weeks, showering at acquaintances’ apartments before finding a room with a creepy older man way out in Queens.

A tech support temp job became permanent, and there I befriended consultants who taught me marketable coding—Classic ASP and SQL Server. We eventually launched Websoft, selling web-based compliance training. We landed Merck Pharmaceuticals, but after paying employees, nothing remained for founders. Despite 100-hour weeks designing and building our entire platform, I came home to an eviction notice.

The Debt Spiral

Partnership fallout left me jobless during the dot-com bust—with my then-girlfriend pregnant. For five devastating months, we lived with her grandmother while she supported us through her vitamin store job. I applied everywhere, facing rejection after rejection. Even simple trips to the grocery store were anxiety-ridden—I’d stand at the checkout, heart racing, hoping the debit card wouldn’t be declined—again. Decades later, I can still vividly remember that sinking feeling. I don’t think I’ll ever forget it.

Eventually, I found work, but from 2001 to 2008, my commutes were brutal—ninety minutes minimum each way, with my longest at 2 hours and 20 minutes each direction. I spent entire potential second jobs just traveling.

The Breaking Point: Debt and Desperation

By 2008, I was training people nationwide in certification programs, gone from my then wife and young daughters for weeks at a time, working 14-hour days, seven days straight. My 2005 house, bought at $205,000 on an interest-only loan, had plummeted to $169,000 by 2013. Credit cards became my false lifeline. I’d feel rushes of relief when credit card companies kept raising my limits—not realizing that they weren’t throwing me a rope to climb out of the hole I was in; they were tossing me a bigger shovel to dig myself even deeper. Each time my limit increased—always accompanied by interest rates well north of 20%—I saw it as an opportunity rather than the trap it truly was. Around this time, I created a spreadsheet to help us track bills against paychecks and get our first view of just how staggeringly bad our debt was. We were over $110,000 in the hole—the same as my entire annual salary at that point.

A New Chapter: Corporate Climb, Financial Fall

Then a former Websoft colleague recruited me to Microsoft. We moved from New Jersey to Bellevue, Washington—but despite the salary bump, my credit was so destroyed we couldn’t qualify for a mortgage. My family lived in an apartment while I worked for one of the world’s richest companies.

Over twelve years at Microsoft, AOL, Verizon, and Yahoo, my salary climbed above $250,000 annually. Despite my high earnings, the corporate culture left me miserable, and I sought happiness in material things—a mistake. My wife and I divorced in this period, and while financial stress didn’t drive us apart, it didn’t make life easier either. Today, my ex-wife and I are on great terms—she’s even a beta-tester for Money@—but back then, the debt was mine to tackle. After separating, I quickly fell back to $57,000 in debt, a painful reminder of how far I’d strayed from my goals and dreams. This setback forced me to recommit to the disciplined financial system I’d begun building. I finally paid it off around the time they laid me off.

December 31, 2023 marked my corporate exit. I’ve worked far harder since then, though I’ve earned just one $2,000 check for marketing services.

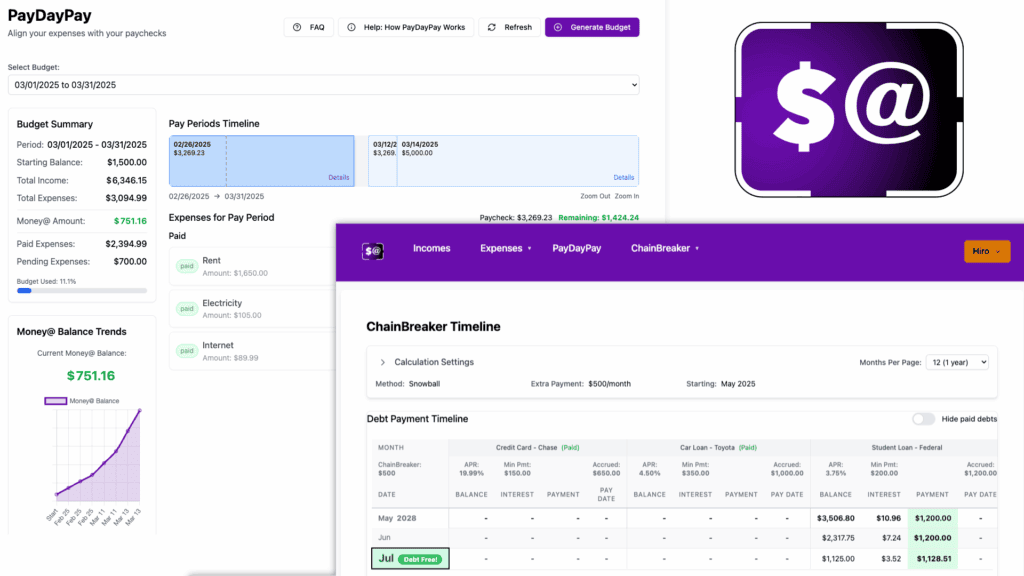

Creating a Lifeline: The Birth of Money@

Through it all, I built Money@—first as my personal salvation system, tracking every dollar and methodically eliminating high-interest debt. It worked. I’ll never forget the euphoria of applying my annual bonus to a credit card and watching a balance that had been in the tens of thousands drop to zero for the first time in years. It was a small win, but it felt like a massive victory. Eventually, I paid off $110,000 in debt, freeing myself to support my aging mother and my four children, meet my family obligations, and make choices based on purpose, not desperation.

Living with Deliberate Freedom

That’s Deliberate Freedom—the power to shape your life through systematic debt elimination and intentional money management. If you’re talented but trapped, earning but drowning, I built this system for you. Because financial freedom isn’t just about having money; it’s about having choices.

From a long ways down a dirt road in the Ozarks, where survival meant milking cows, canning vegetables, and bucking hay for nickels, I learned resilience and self-sufficiency. Now, I live with Deliberate Freedom. I’ve built a life where I can live for what I believe in—supporting my family, making choices driven by purpose and principle, not debt and obligation. Ironically, I’m now searching for a house and acreage, up here in “Live Free or Die” New Hampshire.

Your Turn: Start Your Journey

Ready to break free from debt’s stranglehold and live with Deliberate Freedom? Start small: track every dollar you earn and spend, just as I did. Want to learn how the Money@ system can help you take control? Visit https://mymoneyat.com for tools, tips, and the system that turned my life around.